They take the help of some prominent elements such as labor, material, and miscellaneous expenses to calculate the total costs. Moreover, the above elements are costs for a company that can either be direct or indirect. The modern classification of accounts gives way to several kinds of costs. The debit and credit rules are applied correctly when the type of account is accurately identified.

- In accounting, details are everything, so be sure to make a note of these if you’re planning on doing your own accounting and bookkeeping.

- Representative personal accounts represent a certain person or a group.

- Jami Gong is a Chartered Professional Account and Financial System Consultant.

- Any time your business spends money, your expense accounts increase.

- Only when accounts are set up in the COA can they be selected and used to track specific transactions or financial events in accounting systems.

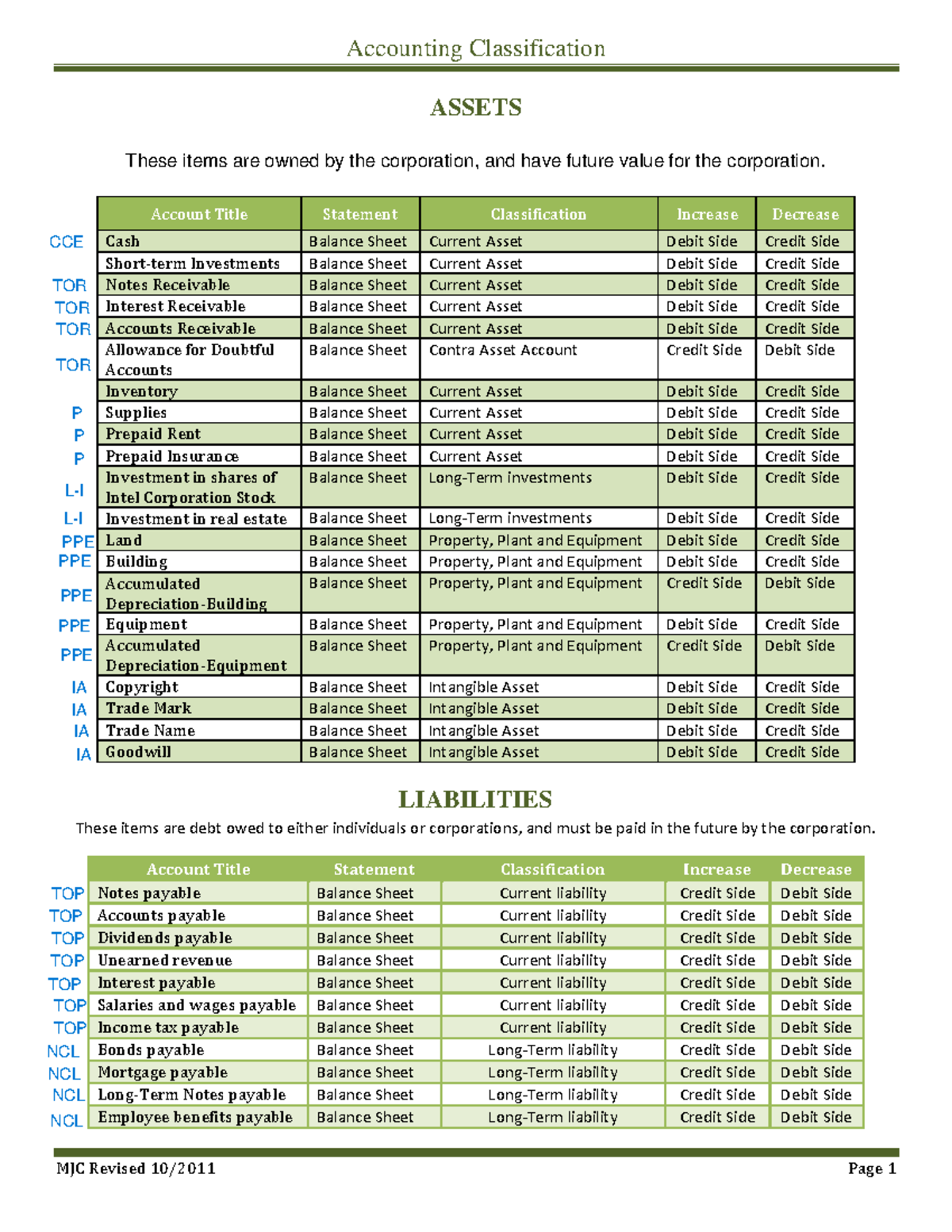

Types of Accounts: Modern and Traditional Classifications

This is a much faster method than scrolling through numerous transactions in the Travel Expenses account, trying to distinguish which are meals and which are flights. Classification of accounts in the ledgers is needed to create the Financial Statements. If the sale and purchase of assets have been properly recorded, that makes it easier to see asset classifications you need to report on the balance sheet. Normally, nominal accounts are used to accumulate income and expense data. In turn, these data can be used to prepare income statements or trading and profit and loss accounts.

Different Types of Accounts in Accounting

But Super Micro’s stock has failed to reverse course on a weak outlook, posing a risk Nasdaq Inc. will delist the company and it will leave the S&P 500 index. (viii) AS 29, Provisions, Contingent Liabilities and Contingent Assets (revised 2016) MSMEs may not comply with paragraphs 66 and 67 relating to disclosures. turbotax and handr block fix irs error delaying stimulus checks to some customers Consequently, if such MSME chooses to measure the ‘value in use’ by not using the present value technique, the relevant provisions of AS 28, such as discount rate etc., would not be applicable to such an entity. Further, such an entity neednot disclose the information required by paragraph 121(g) of the Standard.

Types of Costs and Their Details

One of the main objectives of Accounting is to provide the information for filling up the tax every year. Returns-of-income tax, wealth tax, sales tax, GST, etc should be taken into consideration. For more information about accounting, we can also see the vedantu website and app which provide study materials having full clarity about each concept. Students can also prepare for the examinations from practice questions. Cash is a Real account so Dr. what comes in (9,500), Discount Allowed A/c is a Nominal account so Dr. all expenses/losses (500), and Unreal Co.

Representative Personal Account

Note that every business will have a different chart of accounts based on its business activities. Any transaction posted to the general ledger control account would also be posted to the correct subsidiary ledger account. Thus, the control account and the subsidiary ledger always match. Because the general ledger account is a chronological listing of every transaction, it would be very difficult to find how much a particular customer owes at any given moment. The three main kinds of ledger accounts are the general ledger, the sales ledger, and the purchase ledger. The sales ledger reflects your Accounts Receivable, while the purchase ledger shows Accounts Payable.

In the case of International public companies, international financial reporting standard is applicable together with GAAP. Some people get confused when they see Accounts Receivable since they don’t physically have that money on hand. But because that money is still owed to you, it counts toward your assets.

Your income accounts track incoming money, both from operations and non-operations. Accounts payable (AP) are considered liabilities and not expenses. Because accounts payables are expenses you have incurred but not yet paid for. The bank account is a real account but not a personal or nominal one.

Management Accounting or Managerial Accounting helps managers to make and implement business policies for better results. Cost accounting is a process of recording, summarizing, analyzing, and allocating the cost over the process of manufacturing a product or providing services. There are three different classes of accounting which are Financial Accounting, Cost Accounting, and Management Accounting. Further, they have different results as well as recording and maintenance. Let us understand elaborately the classification of accounting.

The accounts related to incomes, gains, expenses and losses are classified as nominal accounts. These accounts normally serve the purpose of accumulating data needed for preparing income statement or profit and loss account of the business for a particular period. Examples of nominal accounts include sales account, purchases account, wages account, salaries account, interest account, rent account, gain on sale of fixed assets account and loss on sale of fixed assets account etc. A few examples of real accounts are facets of business like cash, land plant, and machinery, examples of personal accounts are like Preeti, Pankaj examples of nominal accounts are like salaries, wages, sales, and purchase.

In sole proprietorship, a single capital account titled as owner’s capital account or simply capital account is used. In partnership or firm, each partner has a separate capital account like John’s capital account, Peter’s capital account etc. In corporate form of business there are many owners known as stockholders or shareholders and the title capital stock account is used to record any change in the capital. For the purpose of applicability of Accounting Standards, Non-company entities are classified into two categories, viz., Micro, Small and Medium Sized Entities (MSMEs) and Large entities.

Try to memorize this chart so that you don’t struggle to categorize your sub-accounts properly. A personal account is created and used for the personal needs of a single person, and an impersonal account can be shared with other people. A special board committee found “no evidence of fraud or misconduct on the part of management or the board of directors,” the company said Nov. 5.